Prototyping and Testing: Ensuring Product-Market Fit

To perfect product-market fit, banks must commit to a cycle of prototyping and testing, the basis of Design Thinking. For instance, they might deploy ML-driven predictive analytics in a prototype to anticipate customer spending patterns in a youth banking vertical. They can test distributed ledger protocols in small-scale remittance services to ensure seamless international transactions for migrant worker segments. Continuous UX testing provides a feedback loop, refining customer interaction touchpoints. This rigorous process helps banks to evolve beyond traditional offerings, creating tailored solutions for verticals such as retirement planning for an aging population, or financing platforms for renewable energy projects, ensuring each solution is a hand-in-glove fit for its intended audience.

Building a Business Case

In addition to prototyping unique banking solutions, it’s essential to construct a robust business case. This involves a thorough analysis of potential costs, including technology development, marketing, staffing, and operational expenses. Alongside, there should be a realistic estimation of revenue generation, considering factors like market size, customer adoption rates, and pricing strategies. This financial evaluation is crucial to ascertain the viability of the new vertical. It provides a clear picture of whether the anticipated returns justify the investment, ensuring that the venture is not only innovative and customer-centric but also financially sustainable.

Build, Buy, Partner: Navigating Implementation Choices and Challenges

In the strategic journey of vertical expansion, traditional banks face a crucial decision: whether to build, buy, or partner for implementing new solutions. This choice is pivotal, especially for legacy banks grappling with the agility of modern banking demands.

Building in-house offers complete control and alignment with the bank’s unique processes and culture but may be hindered by time-consuming development and rigid legacy IT systems. This approach allows for custom-tailored solutions but requires significant investment in resources and time for maintenance and upgrades.

On the other hand, buying solutions can accelerate the market entry process. It provides access to ready-made, tested technologies, reducing development time and resource allocation significantly. However, this might lead to compromises in terms of integration with existing systems and the level of customization possible, potentially leading to a solution that doesn’t entirely align with the bank’s vision or customer needs.

Partnering with fintech companies presents a balanced approach, combining the agility, innovation, and technological advancement of fintechs with the robust infrastructure and customer base of traditional banks. This collaboration allows for rapid deployment of new technologies and facilitates adaptation to evolving market demands. Partnering can also spread out risks and costs, making it a more viable financial option, especially when venturing into untested markets or developing cutting-edge solutions.

The decision-making process should involve a comprehensive assessment of the bank’s strategic long-term goals, the urgency of market entry, available resources, and how well each option aligns with customer expectations and market trends. This decision will significantly influence the bank’s ability to effectively and efficiently roll out new verticals, ensuring they meet the evolving needs of their target market while staying ahead in the competitive financial landscape.

Financial Planning and Risk Management for New Verticals

In the quest to architect new verticals within the banking sector, financial planning and risk management become the twin pillars upon which sustainable growth is built. Through meticulous budgeting and forecasting, banks can chart financial blueprints that align with strategic objectives. This involves determining the costs associated with technology integration, market entry, and ongoing operations, while also forecasting potential revenue streams. Especially since the time and money that needs to be invested for Know-your-Customer tasks are getting more expensive for traditional banks.

But besides financial planning, the regulatory landscape for banks isn’t getting easier to traverse! Banks must proactively address these challenges, staying informed about regulatory changes and understanding the compliance intricacies of each new vertical. This proactive stance enables banks to navigate the complexities of compliance without stifling innovation, ensuring that new offerings are not only pioneering but also fully compliant.

Next to managing regulatory risks and challenges come the normal banking risks that still need to be assessed. This means conducting thorough risk assessments for each vertical, evaluating market risks, operational risks, credit risks, and beyond. By preempting these risks and developing strategies to mitigate them, banks can safeguard their ventures, ensuring the stability and integrity of their vertical expansions.

Branding, Marketing, and Positioning to new Vertical

In the vibrant landscape of vertical banking, branding, marketing, and positioning form the cornerstone of a bank’s journey into new and specialized market segments. This expanded section delves into the intricacies of these three critical components, vital for the successful launch and sustenance of a banking vertical.

Establishing a Strong Brand Identity: Distinct and Memorable

A powerful brand identity is not merely about visual aesthetics; it’s about creating an emotional resonance with the target audience. It should encapsulate the core promise of the vertical, its ethos, and its unique value proposition. This identity must be consistent across all platforms, from digital to print, ensuring that the vertical is instantly recognizable. It’s about forging a connection that goes beyond transactional relationships to create a sense of belonging and trust. The identity should reflect not just what the bank offers but also what it stands for, making it a symbol of the specific aspirations and values of its target audience.

Crafting a Marketing Strategy: Reaching the Target Audience Effectively

An effective marketing strategy in vertical banking is akin to a well-orchestrated symphony. It must harmonize various elements – from digital marketing techniques like SEO, content and social media campaigns to traditional methods such as community engagement and print advertising. This strategy should tell a compelling story, one that weaves the offerings of the vertical into the daily lives of its target audience. It should leverage data analytics to understand customer preferences and behaviors, allowing for personalized and targeted marketing efforts.

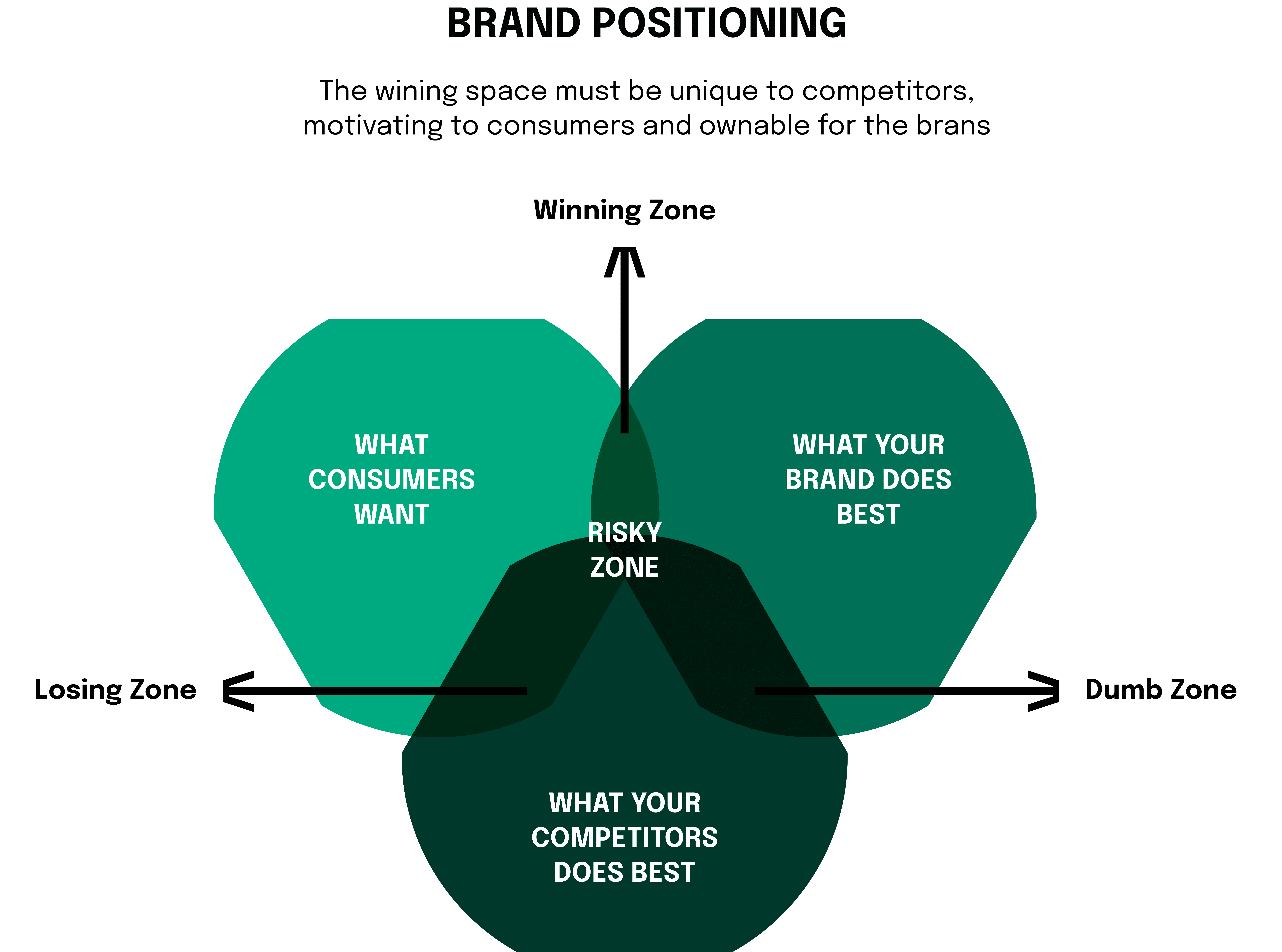

Positioning in the Competitive Landscape: Differentiating the Offering

Positioning the new vertical in a crowded market demands a strategic approach. It involves identifying and articulating a unique selling proposition (USP) that sets the vertical apart. This USP could be an innovative product feature, exceptional customer service, or a commitment to certain values like sustainability or inclusivity. The positioning should be clear and compelling, highlighting the benefits and value that the vertical brings to its customers. It’s about creating a narrative that not only differentiates but also elevates the vertical in the eyes of the target audience.

In an era of banking transformation, the call for vertical banking solutions has become a clarion for innovation. As incumbent banks cast their sight towards a future sculpted by meticulous user experience (UX), they find themselves at the start of a financial renaissance. This evolution is underscored by the need to craft banking experiences that not only serve but delight—a user-centric design that is no longer a luxury but an imperative. New verticals are just not only a channel anymore, banks must see them as unique products with major business opportunities. If it is just seen as a digital channel, verticals are treated as “features” or an afterthought. To counteract this view, this article creates a holistic approach of how to build verticals and how to launch them to cater to new consumer needs!

In an era of banking transformation, the call for vertical banking solutions has become a clarion for innovation. As incumbent banks cast their sight towards a future sculpted by meticulous user experience (UX), they find themselves at the start of a financial renaissance. This evolution is underscored by the need to craft banking experiences that not only serve but delight—a user-centric design that is no longer a luxury but an imperative. New verticals are just not only a channel anymore, banks must see them as unique products with major business opportunities. If it is just seen as a digital channel, verticals are treated as “features” or an afterthought. To counteract this view, this article creates a holistic approach of how to build verticals and how to launch them to cater to new consumer needs!